Via Accounting Today

Doeren Mayhew was recognized as one of the Accounting Today's 2012 Top 100 Firms

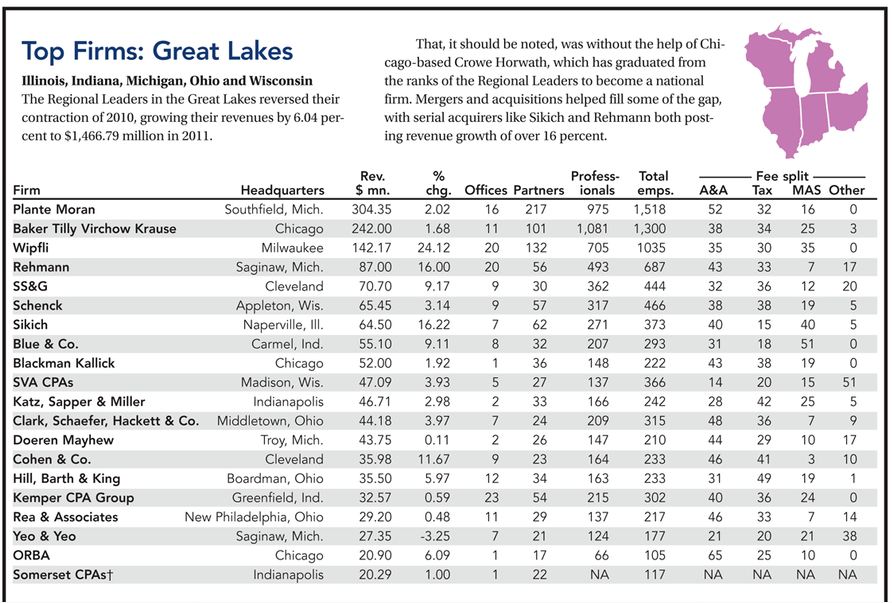

Accounting Today - Top Firms 2012 - Doeren Mayhew

Accounting Today - Top Firms 2012 - Doeren Mayhew - Regional Firms

| Doeren Mayhew | |

IRS extends deadline for estate tax portability election

The Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010 (2010 Tax Relief Act) provided that for decedents dying in 2011, the first $5 million of his or her estate's gross assets would be excluded from the estate tax. If the first spouse of a married couple died in 2011 with a taxable estate worth less than $5 million, the estate would have an unused estate tax exclusion, which it could elect to transfer to the surviving spouse. This "portability election" generally is available if the first spouse dies in 2011 or 2012; the latest extension applies to estates of decedents who died in the first six months of 2011. Following enactment of the 2010 Tax Relief Act, however, the IRS did not come out with guidance (Notice 2011-82) on portability until the end of September, 2011. With estate tax returns due nine months after death, this provided little time for estates to comply with the election requirements. As an answer to this problem, the IRS extended the deadline for certain estates to make a portability election that would allow the surviving spouse to use the remaining amount from the estate and gift tax exclusions of the spouse that was first to die. I am a surviving spouse. How do I make the election? To make the election that would allow the surviving spouse to use the unused exclusion of the deceased spouse, the estate of the deceased spouse must timely file (including extensions) Form 706, the estate tax return. The Form 706 must include a computation of the unused exclusion amount. The portability election can only be made by filing Form 706. How do I obtain an extension of time to file? Estates can obtain a six-month extension of time to file the estate tax return (giving them a total of 15 months), by submitting Form 4768, Application for Extension of Time To File a Return and/or Pay U.S. Estate Tax. Form 4768 must be filed within nine months after death to obtain the additional six-month extension. The extension is available to a qualifying estate, where:

IR-2012-24, Notice 2012-21 Contact Doeren Mayhew for more information.

|

Doeren Mayhew | |

Disregarded entities cannot have multiple interests

Limited liability companies (LLCs) are becoming more popular. If the LLC has only one owner, the owner can elect whether to treat the LLC as a disregarded entity (DE) for federal tax purposes or as an association taxable as a corporation. DE treatment for the LLC may be particularly appealing because the owner has the benefit of passthrough taxation, like a partnership, but with limited liability, like a corporation. With only one interest outstanding, the DE generally has a simplified ownership structure. An IRS Chief Counsel memorandum has now addressed the situation where a taxpayer established a DE with multiple ownership interests under state law. The DE split its ownership interest into separate classes of membership interests. However, the sole owner retained ownership of all interests. The DE then allocated income, loss, deduction, credit and basis among the classes of interests, for federal tax purposes. By doing this, the owner attempted to create an "outside" basis in the DE and to control the recognition of income or loss from distributions by the entity or dispositions of an interest in the entity. Chief Counsel concluded that the multiple interests have no effect under federal tax law. The owner does not own a separate class of interests in the DE. Instead, the owner is treated as directly owning each of the DE's assets, like a sole proprietorship, branch, or division of the owner. A DE cannot have multiple interests for tax purposes. The owner already owns all of the DE's property. Attempts to allocate items to the owner's different interests have no meaning under federal tax law, when the same person owns 100 percent of all classes of interests. A distribution by the entity, or the "disposition" of an interest in the entity, has no independent significance. LLCs, nevertheless, remain an excellent form of ownership for many single-owner businesses, providing significant tax planning opportunities. Our office is here to advise you on what can and cannot be done. Contact Doeren Mayhew for more information.

|

| Doeren Mayhew | |

Overwhelming majority believe tax compliance is civic duty

Since 2002, the IRS Oversight Board has conducted an annual survey of American taxpayers and their views on IRS administration and tax compliance. This year's survey, conducted for the 2011 tax year, reveals that 72 percent of Americans view accurately complying with tax law as their civic duty. The number of taxpayers who believe that paying income tax is their civic duty increased by three percentage points from 2010. The percentage of taxpayers, however, who believe it is acceptable to cheat "as much as possible" on their returns increased by four percentage points from last year, and the percentage of taxpayers who believe it is not at all acceptable to cheat on income taxes decreased by three percentage points, returning to its 2009 level. Personal integrity inspires compliance Personal integrity was the factor that taxpayers said most influenced their decision to honestly report their income for tax purposes. Seventy-nine percent of taxpayers told the Board that personal integrity has a "great deal of influence" on their compliance. Third party reporting of financial information influenced approximately 65 percent of taxpayers; and fear of an audit influenced just over 59 percent of taxpayers to comply. Public frequently uses IRS tools The Board also described taxpayer attitudes toward IRS customer services, such as its toll-free telephone helpdesk, the agency's website, and e-filing opportunities. Seventy-four percent of those surveyed rated the IRS toll-free customer service number as "very important," which represented a slight decrease from 2010. Additionally, 70 percent of taxpayers rated the IRS website as "very important," the same figure as reported last year. Sixty-eight percent of taxpayers reported that having opportunities to electronically file their returns was "very important," representing a one-percentage point decrease from 2010. Taxpayer services that appeared less important included the ability to email the IRS directly with questions (rated as "very important" by 47 percent of taxpayers). Also less important were community-based tax clinics (26 percent rated them "very important"), tax assistance vans at locations far from IRS offices, and computer terminals located at a library or shopping mall. IRS Oversight Board, 2011 Taxpayer Attitude Survey, January 30, 2012 Contact Doeren Mayhew for more information.

|

| Doeren Mayhew | |

New FATCA regulations shine brighter spotlight on foreign accounts

The IRS has issued long-awaited comprehensive proposed regulations to implement the Foreign Account Tax Compliance Act (FATCA). Because FATCA is scheduled to take effect January 1, 2013, the government will move quickly to obtain comments from the public, hold a public hearing, and issue final regulations. Reporting/withholding FATCA requires foreign financial institutions (FFIs) and other entities to report information to the IRS about foreign accounts and assets owned by U.S. taxpayers. If the accounts are not properly disclosed to the IRS, FATCA requires 30 percent withholding on payments made to the accounts. FATCA is a complex statute that imposes new obligations on FFIs and other entities. These obligations directly impact the account holders, whether they are individuals, businesses, or trusts. To ease the transition to the new regime, the IRS will implement FATCA in phases. For example, only identifying information and account balance or value would need to be reported in 2014 (with respect to 2013 accounts). Delayed deadlines To allow entities to make the systems adjustments needed to report income and gross proceeds, the IRS would not require the reporting of account income until 2016 (with respect to the 2015 calendar year), and would not require reporting of gross proceeds (from the sale of account assets) until 2017 (with respect to the 2016 calendar year). The proposed rules also grandfather obligations outstanding on January 1, 2013 from reporting and withholding requirements. Stakeholders have hailed the IRS for being responsive to concerns. For example, in addition to the transition rules, the IRS eased up on the due diligence requirements for FFIs and other entities to review accounts and identify U.S. taxpayers with an interest in the account. The IRS stated that it sought to retain the goals and purposes of FATCA, while reducing the burden on implementing its requirements. Treasury also announced that it had proposed an alternative system - an intergovernmental approach that would allow FFIs to report information to their own home governments. The governments in turn would report the information to Treasury. Five European governments have agreed to this approach; Treasury will continue to discuss the proposal with additional countries. Accountholder responsibilities Irrespective of the reporting or withholding obligations of FFIs, account holders continue to have a current obligation to report their accounts and declare any U.S. income tax due on them. There are significant penalties imposed for ignoring those requirements. Please contact Doeren Mayhew if you need assistance.

|

| Doeren Mayhew | |

IRS to increase compliance through greater certainty/efficiency/cooperation

The IRS is mitigating administrative tax risk to both taxpayers and the government by fostering greater certainty, consistency and efficiency in its programs and policies, Commissioner Douglas Shulman said in his keynote speech at the The Tax Council Policy Institute's recent symposium in Washington, D.C. in mid-February. There are numerous programs already in effect through which taxpayers can communicate and work effectively with the IRS to clarify tax regulations, avoid or expedite audits, or otherwise increase compliance. These include the Compliance Assurance Process (CAP) program, which enables large corporate taxpayers to work on their returns with the IRS to resolve issues before filing; the Industry Issue Resolution (IIR) Program designed to resolve issues affecting numerous business taxpayers; the Fast Track Settlement, designed to streamline the audit process in a mediation setting; and the Uncertain Tax Position Initiatives through which large corporations report tax positions that affect their U.S. tax liabilities. Shulman also stated that new guidance could often be instrumental in providing certainty for tax planners. He cited the example of the recent proposed regs that are intended to mitigate the restrictive required minimum distribution requirements from longevity annuities. "This guidance actually reduced uncertainty for a whole product class that could be used to help our seniors manage making sure that they don't run out of money in retirement." International cooperation Shulman highlighted the role of greater cooperation between international tax administrations in increasing compliance and reducing taxpayer burden in a multinational setting. Shulman cited an example of a joint audit conducted alongside a foreign tax administration. The audit and negotiations for the advance pricing agreement took six months rather than several years and, in the end, resulted in certainty for the taxpayer with respect to its future tax payments in all the relevant jurisdictions. Tax administration Meanwhile, IRS Deputy Commissioner for Services and Enforcement Steven Miller said the IRS has become more efficient, although it still seeks to improve its activity in transfer pricing and offshore enforcement. The IRS may also increase enforcement in passthrough entities and financial products. In order to facilitate enforcement, the IRS may use certain data, such as that gleaned from credit card transactions and the information reported pursuant to the Foreign Account Tax Compliance Act (FATCA). The IRS will likely also leverage third party sources, such as tax preparers and whistleblowers, to aid compliance. Whistleblowers are a large boon to coporate tax compliance, with 44 percent of whistleblowers involving large corporate taxpayers. Contact Doeren Mayhew for more information.

|

| Doeren Mayhew | |

MI - Tax tribunal abused its discretion by dismissing taxpayers' petition

Contact Doeren Mayhew for more information.

|

| Doeren Mayhew | |

Coming soon: greater tax-wise retirement options

Retired employees often start taking benefits by age 65 and, under the minimum distribution rules, must begin taking distributions from their retirement plans when they reach age 70 1/2. According to Treasury, a 65-year old female has an even chance of living past age 86, while a 65-year old male has an even chance of living past age 84. The government has become concerned that taxpayers who normally retire at age 65 or even age 70 will outlive their retirement benefits. The government has found that most employees want at least a partial lump sum payment at retirement, so that some cash is currently available for living expenses. However, under current rules, most employer plans do not offer a partial lump sum coupled with a partial annuity. Employees often are faced with an "all or nothing" decision, where they would have to take their entire retirement benefit either as a lump sum payment when they retire, or as an annuity that does not make available any immediate lump-sum cash cushion. For retirees who live longer, it becomes difficult to stretch their lump sum benefits. Longevity solution To address this dilemma, the government is proposing new retirement plan rules to allow plans to make available a partial lump sum payment while allowing participants to take an annuity with the other portion of their benefits. Furthermore, to address the problem of employees outliving their benefits, the government would also encourage plans to offer "longevity" annuities. These annuities would not begin paying benefits until ages 80 or 85. They would provide you a larger annual payment for the same funds than would an annuity starting at age 70 1/2. Of course, one reason for the better buy-in price is that you or your heirs would receive nothing if you die before the age 80 or 85 starting date. But many experts believe that it is worth the cost to have the security of knowing that this will help prevent you from "outliving your money." To streamline the calculation of partial annuities, the government would allow employees receiving lump-sum payouts from their 401(k) plans to transfer assets into the employer's existing defined benefit (DB) plan and to purchase an annuity through the DB plan. This would give employees access to the DB plans low-cost annuity purchase rates. According to the government, the required minimum distribution (RMD) rules are a deterrent to longevity annuities. Because of the minimum distribution rules, plan benefits that could otherwise be deferred until ages 80 or 85 have to start being distributed to a retired employee at age 70 ½. These rules can affect distributions from 401(k) plans, 403(b) tax-sheltered annuities, individual retirement accounts under Code Sec. 408, and eligible governmental deferred compensation plans under Code Sec. 457. Tentative limitations The IRS proposes to modify the RMD rules to allow a portion of a participant's retirement account to be set aside to fund the purchase of a deferred annuity. Participants would be able to exclude the value of this qualified longevity annuity contract (QLAC) from the account balance used to calculate RMDs. Under this approach, up to 25 percent of the account balance could be excluded. The amount is limited to 25 percent to deter the use of longevity annuities as an estate planning device to pass on assets to descendants. Coming soon Many of these changes are in proposed regulations and would not take effect until the government issues final regulations. The changes would apply to distributions with annuity starting dates in plan years beginning after final regulations are published, which could be before the end of 2012. Doeren Mayhew will continue to monitor the progress of this important development.

|

| Doeren Mayhew | |

Administration unveils Framework for Business Tax Reform

The Framework contains a large number of general business-oriented proposals which, according to the administration, will make the Tax Code less complicated for businesses and increase the nation's competitiveness in the global economy. A reduction in the corporate tax rate would be fully paid for by repeal of business tax preferences. The Framework also calls for a new minimum tax on overseas profits and encourages companies to return work to the U.S. by offering a new relocation tax incentive. Congressional reaction to the administration's Framework was mixed. Democrats in Congress generally applauded the Framework for laying out a plan to reduce the corporate tax rate, a proposal that enjoys bipartisan support in Congress. Republicans were less enthusiastic, but some GOP lawmakers said that the Framework could serve as a starting point for comprehensive tax reform. While the November elections certainly play a part in the release of the current proposals, major tax reform now is considered inevitable by most observers. The question remains, however, as to how it will develop over the coming months. Five-part framework The President's overall proposal, which currently is framed only in general terms, is grounded in five elements: --Eliminating tax expenditures and subsidies, broadening the corporate tax base, and cutting the corporate tax rate from 35 percent to 28 percent; --Strengthening U.S. manufacturing and innovation by effectively lowering the rate for manufacturers to 25 percent (through an enhanced manufacturing credit), making the research tax credit permanent, and providing a number of clean-energy incentives; --Fixing the international tax system that includes imposing a minimum tax on overseas profits, creating a 20 percent tax credit for moving operations back to the U.S., denying deductions for moving operations overseas, limiting the transfer of patents and other intellectual property to offshore subsidiaries, and delaying deductions for interest paid for overseas investments; --Simplifying and cutting taxes for small businesses (not just for corporations) through a number of reforms, including a 100 percent expensing up to $1 million; cash accounting for businesses with gross receipts up to $5 million; enhanced deductions for startup expenses, and an enhanced Code Section 45R small employer health insurance tax credit; and --Restoring fiscal responsibility and not add to the deficit through making reform revenue neutral, including a need to do so for whatever portion of the $250 billion in reoccurring extender tax benefits that Congress deems necessary to continue. Individual tax reform In unveiling this framework for business tax reform, Treasury Secretary Timothy Geithner stated that individual tax reform does not necessarily need to be considered at the same time as business tax reform. With individual tax reform clearly the most politically volatile component to total tax reform, most Washington observers believe that tax reform will follow a sequential route, with business tax reform going first. Contact Doeren Mayhew for more information.

|

| Doeren Mayhew | |

How do I... Guard against taxpayer identity theft?

In light of these dangers, the IRS has taken numerous steps to combat identity theft and protect taxpayers. There are also measures that you can take to safeguard yourself against identity theft in the future and assist the IRS in the process. IRS does not solicit financial information via email or social media The IRS will never request a taxpayer's personal or financial information by email or social media such as Facebook or Twitter. Likewise, the IRS will not alert taxpayers to an audit or tax refund by email or any other form of electronic communication, such as text messages and social media channels. If you receive a scam email claiming to be from the IRS, forward it to the IRS at phishing@irs.gov. If you discover a website that claims to be the IRS but does not begin with 'www.irs.gov', forward that link to the IRS atphishing@irs.gov. How identity thieves operate Identity theft scams are not limited to users of email and social media tools. Scammers may also use a phone or fax to reach their victims to solicit personal information. Other means include: -Stealing your wallet or purse -Looking through your trash -Accessing information you provide to an unsecured Internet site. How do I know if I am a victim? Your identity may have been stolen if a letter from the IRS indicates more than one tax return was filed for you or the letter states you received wages from an employer you don't know. If you receive such a letter from the IRS, leading you to believe your identity has been stolen, respond immediately to the name, address or phone number on the IRS notice. If you believe the notice is not from the IRS, contact the IRS to determine if the letter is a legitimate IRS notice. If your tax records are not currently affected by identity theft, but you believe you may be at risk due to a lost wallet, questionable credit card activity, or credit report, you need to provide the IRS with proof of your identity. You should submit a copy of your valid government-issued identification, such as a Social Security card, driver's license or passport, along with a copy of a police report and/or a completed IRS Form 14039, Identity Theft Affidavit, which should be faxed to the IRS at 1-978-684-4542. What should I do if someone has stolen my identity? If you discover that someone has filed a tax return using your SSN you should contact the IRS to show the income is not yours. After the IRS authenticates who you are, your tax record will be updated to reflect only your information. The IRS will use this information to minimize future occurrences. What other precautions can I take? There are many things you can do to protect your identity. One is to be careful while distributing your personal information. You should show employers your Social Security card to your employer at the start of a job, but otherwise do not routinely carry your card or other documents that display your SSN. Only use secure websites while making online financial transactions, including online shopping. Generally a secure website will have an icon, such as a lock, located in the lower right-hand corner of your web browser or the address bar of the website with read "https://..." rather than simply "http://." Never open suspicious attachments or links, even just to see what they say. Never respond to emails from unknown senders. Install anti-virus software, keep it updated, and run it regularly. For taxpayers planning to e-file their tax returns, the IRS recommends use of a strong password. Afterwards, save the file to a CD or flash drive and keep it in a secure location. Then delete the personal return information from the computer hard drive. Finally, if working with an accountant, query him or her on what measures they take to protect your information. Contact Doeren Mayhew for more information.

|

| Doeren Mayhew | |

FAQ: What are employer share responsibility assessable payments under the PPACA?

Shared responsibility payment The PPACA imposes a shared responsibility assessable payment on certain large employers (Code Sec. 4980H). The provisions about shared responsibility for large employers are among the most complex in the PPACA. Generally, a large employer will be subject to an assessable payment if any full-time employee is certified to receive a premium assistance tax credit and either the employer does not offer full-time employees (and their dependents) the opportunity to enroll in minimum essential coverage under an employer plan (Code Sec. 4980H(a)) or the employer offers full-time employees (and their dependents) the opportunity to enroll in minimum essential coverage that either is unaffordable or does not provide minimum value (Code Sec. 4980H(b)). The shared responsibility payment requirement is scheduled to be effective after 2013. The PPACA describes how to calculate the shared responsibility payment. The annual assessable payment under Code Sec. 4980H(a) is based on all (excluding the first 30) full-time employees. The annual assessable payment under Code Sec. 4980H(b) is based on the number of full-time employees who are certified to receive an advance payment of an applicable premium tax credit. The shared responsibility payment requirement applies to "large" employers. The PPACA describes a large employer as generally an employer that employed an average of at least 50 full-time employees on business days during the preceding calendar year. The PPACA includes special rules for employers that employ seasonal workers. The PPACA exempts small firms that have fewer than 50 full-time employees. More guidance expected In 2011, the IRS, DOL and HHS alerted employers that the agencies would be developing rules and regulations to implement the PPACA's shared responsibility payment requirement. The agencies also requested comments from employers and interested parties. The IRS observed that the definitions of employer and employee are key in determining whether and, if so, to what extent, an employer may incur a shared responsibility payment. The IRS indicated that it would likely define "employer" to mean the entity that is the employer of an employee under the common-law test. Generally, employee would mean a worker who is an employee under the common-law test. An employer's status as a large employer would be based on the sum of full-time employees and full-time equivalent employees, the IRS noted. Keep in mind that the IRS's observations are just that at this time. The IRS has not issued proposed regulations. It is unclear when proposed regulations may be released. Additionally, the Supreme Court has agreed to take up the PPACA and the Court could rule that all or part of the PPACA, including the employer shared responsibility payment, is unconstitutional. Contact Doeren Mayhew for more information.

|

| Doeren Mayhew | |

March 2012 tax compliance calendar

As an individual or business, it is your responsibility to be aware of and to meet your tax filing/reporting deadlines. This calendar summarizes important tax reporting and filing data for individuals, businesses and other taxpayers for the month of March 2012.March 2 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates February 25-28. March 7 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates February 29-March 2. March 9 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates March 3-6. March 12 Employees who work for tips. Employees who received $20 or more in tips during February must report them to their employer using Form 4070. March 14 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates March 7-9. March 15 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates February 8-10. Monthly depositors. Monthly depositors must deposit employment taxes for payments in January. March 16 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates March 10-13. March 21 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates March 14-16. March 23 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates March 17-20. March 28 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates March 21-23. March 30 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates March 24-27. April 4 Employers. Semi-weekly depositors must deposit employment taxes for payroll dates March 28-30. April 6 Employers. Semi-weekly depositors must deposit employment taxes for payroll date of March 31. Doeren Mayhew

|